A new study by The Kaplan Group explores the relationship between generational spending patterns and geographical cost of living. It also examines how location-based cost of living impacts savings potential more significantly than raw income, with lower-cost states demonstrating higher savings scores despite lower median incomes.

Key Takeaways

- Gen X demonstrates the highest potential for savings, with an annual savings potential of $27,200.

- Mississippi leads the state rankings with a 16.7 savings score. This highlights that areas with a lower cost of living offer better savings potential, even when median incomes are lower, such as $45,081 in Mississippi.

- The essential expense ratios decrease consistently with age, from 91.9% for individuals under 25 to 83.8% for those aged 55-64.

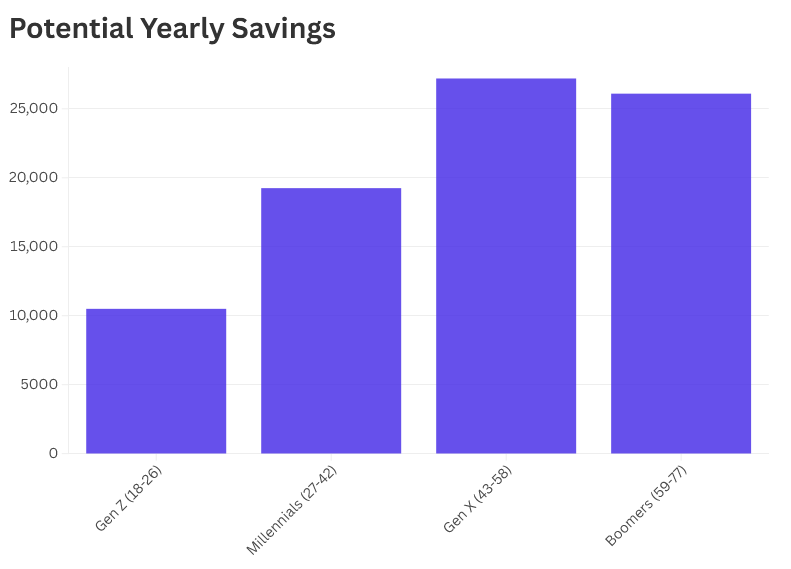

Generational Savings Potential

Generational spending patterns reveal a clear inverse relationship between age and essential expenses ratio, with potential annual savings increasing significantly as generations mature. This suggests that individuals tend to manage their expenses more efficiently as they age, leading to greater savings potential.

Gen X stands out as the best in terms of savings potential, with an impressive annual savings capability of $27,200. On the other hand, Gen Z, despite being at the start of their financial journey, shows the worst savings potential due to a higher essential expenses ratio and lower disposable income. Their annual savings potential is significantly lower, highlighting the challenges faced by younger generations in managing finances. Millennials, positioned between Gen Z and Gen X, represent the average with a moderate savings potential. They are in a transitional phase, improving their financial management skills but still facing challenges in balancing expenses and savings.

State Savings Rankings

Mississippi emerges as the best state for savings potential, boasting a 16.7 savings score. This is attributed to its low cost of living, which allows residents to save more despite having a lower median income of $45,081. Conversely, states with higher costs of living, such as California, often show the worst savings potential due to the high expenses that erode disposable income, even if the median income is higher. Kansas, with a moderate cost of living and a reasonable median income, represents the average, offering a balanced environment for savings. It highlights the importance of considering both income and living costs when evaluating savings potential.

Saving Score by State

| Rank | State | Savings Score | Monthly Savings |

| 1 | Mississippi | 16.7 | 627.37725 |

| 2 | Kansas | 13.5 | 698.47875 |

| 3 | Alabama | 12.1 | 509.5713333 |

| 4 | Oklahoma | 12.1 | 542.8866667 |

| 5 | Missouri | 11.1 | 529.9325 |

| 6 | Georgia | 10.8 | 551.016 |

| 7 | Iowa | 10.1 | 520.453 |

| 8 | Indiana | 10 | 480.025 |

| 9 | Michigan | 9.7 | 478.8081667 |

| 10 | Ohio | 9.2 | 445.556 |

| 11 | Tennessee | 9.1 | 404.3433333 |

| 12 | Arkansas | 8.9 | 363.0606667 |

| 13 | Kentucky | 8.6 | 374.7808333 |

| 14 | Texas | 8.5 | 453.5741667 |

| 15 | Louisiana | 8.2 | 347.1333333 |

| 16 | Nebraska | 8 | 421.5266667 |

| 17 | Wyoming | 7.7 | 417.1025833 |

| 18 | South Carolina | 6.8 | 310.896 |

| 19 | Illinois | 5.5 | 317.1070833 |

| 20 | North Carolina | 5.1 | 243.69925 |

| 21 | Wisconsin | 4.3 | 226.7999167 |

| 22 | Florida | 2.1 | 100.98025 |

| 23 | South Dakota | 1.9 | 94.26058333 |

| 24 | Pennsylvania | 1.7 | 90.13825 |

| 25 | Arizona | 1.6 | 82.03866667 |

| 26 | Minnesota | 1.5 | 93.24125 |

| 27 | North Dakota | 1.3 | 69.95841667 |

| 28 | Virginia | -0.7 | -44.5655 |

| 29 | Nevada | -0.8 | -42.184 |

| 30 | Delaware | -1.2 | -70.176 |

| 31 | New Mexico | -1.3 | -55.51325 |

| 32 | Colorado | -1.9 | -122.11775 |

| 33 | Idaho | -2.1 | -106.74825 |

| 34 | Montana | -2.3 | -109.54325 |

| 35 | Utah | -2.4 | -151.56 |

| 36 | Maine | -3.5 | -171.8616667 |

| 37 | Rhode Island | -4.8 | -281.22 |

| 38 | Vermont | -5.2 | -273.0043333 |

| 39 | New Hampshire | -5.4 | -350.6985 |

| 40 | Washington | -5.5 | -352.9441667 |

| 41 | Connecticut | -6.4 | -446.7786667 |

| 42 | Oregon | -6.8 | -372.113 |

| 43 | New Jersey | -8.5 | -603.81875 |

| 44 | Maryland | -9.4 | -681.9935 |

| 45 | Alaska | -9.6 | -603.704 |

| 46 | Massachusetts | -10.4 | -731.3366667 |

| 47 | New York | -16.3 | -976.2341667 |

| 48 | California | -16.4 | -1075.184 |

| 49 | Hawaii | -16.8 | -1164.422 |

Age and Essential Expenses

The trend of decreasing essential expense ratios with age is most favorable for the 55-64 age group, who have an essential expense ratio of 83.8%. In contrast, individuals under 25 face the worst scenario, with a high essential expense ratio of 91.9%, indicating a struggle to manage expenses effectively. The 35-44 age group represents the average, showing a gradual improvement in financial management as they gain experience and stability. This progression underscores the importance of financial education and experience in achieving better financial outcomes over time.

The study emphasizes the importance of financial management skills and strategic living location choices in enhancing savings potential.

Methodology

Data was sourced from the Bureau of Labor Statistics (BLS) Consumer Expenditure Survey (2022) and analyzed to calculate essential expense ratios, savings scores, and generational savings potential. The state savings ranking methodology evaluates states based on their cost of living index, median income, and essential expenses ratio, with states like Mississippi achieving high savings scores (16.7%) due to lower living costs. Analytical techniques included regression and comparative analysis to identify trends and insights.